Your credit utilization rate is a key metric that reflects how much of your available revolving credit you’re currently using. Expressed as a percentage, it’s calculated by dividing the total balance of your revolving credit accounts by their combined credit limits. This figure is a critical factor in determining your credit score, influencing your ability to secure loans, credit cards, or favorable interest rates. Keeping your utilization rate low is a cornerstone of sound financial management. In this article, we’ll break down everything you need to know about credit utilization, how it’s calculated, and actionable strategies for maintaining an optimal rate to boost your credit health.

The credit utilization rate, also referred to as the credit utilization ratio, measures the portion of your revolving credit you’re actively using compared to what’s available to you. Revolving credit includes accounts like credit cards or lines of credit, where you can borrow repeatedly up to a set limit. A lower utilization rate is generally associated with higher credit scores, signaling to lenders that you manage credit responsibly. Understanding and controlling your utilization rate is essential for improving your financial standing and unlocking better credit opportunities.

What Goes Into Calculating Your Credit Utilization Rate?

Your credit utilization rate is calculated based on revolving credit accounts, which differ from installment loans like mortgages or auto loans. The specific accounts considered in the calculation may vary slightly depending on the credit scoring model, but they typically include:

Credit Cards: Both primary accounts and those where you’re an authorized user.

Personal Lines of Credit: Flexible borrowing options like unsecured lines of credit.

Home Equity Lines of Credit (HELOC): Credit secured by your home’s value.

Closed Revolving Accounts with Balances: Accounts you’ve closed but still owe money on.

The balances and credit limits used in the calculation come from your credit report, which may not always reflect your current account status due to reporting delays. This distinction is important when assessing your utilization rate.

Calculating your credit utilization rate is a straightforward process that empowers you to monitor your credit health. Follow these steps:

Gather Balances and Credit Limits: Obtain the balances and credit limits for all your revolving accounts from your credit report.

Sum the Totals: Add up the total balances across all revolving accounts and the total credit limits.

Perform the Calculation: Divide the total balance by the total credit limit, then multiply by 100 to get the percentage.

For instance, imagine you have three credit cards: one with a $4,000 balance and $8,000 limit, another with a $1,000 balance and $5,000 limit, and a third with a $0 balance and $7,000 limit. Your total balance is $5,000, and your total credit limit is $20,000. Dividing $5,000 by $20,000 and multiplying by 100 gives you a 25% utilization rate.

Your overall credit utilization rate provides a big-picture view, but individual account utilization rates also matter. Using the previous example, the first card has a 50% utilization rate ($4,000 ÷ $8,000), the second has 20% ($1,000 ÷ $5,000), and the third has 0% ($0 ÷ $7,000).

Credit scoring models often consider both your overall rate and the highest utilization rate on any single account. A card with a high utilization rate, such as 90% or 100%, can negatively impact your score, even if your overall rate is low. Monitoring both metrics is crucial for maintaining a strong credit profile.

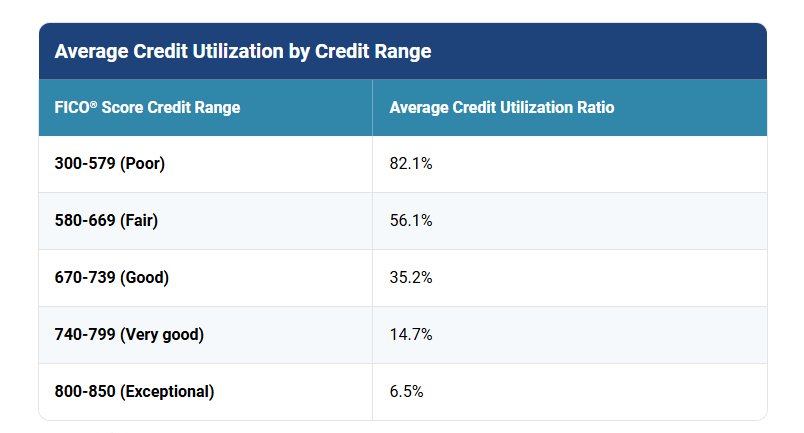

A good credit utilization rate is a low one. According to Experian data from Q3 2022, the average U.S. credit utilization rate was 28%. However, those with excellent credit scores (e.g., FICO scores above 800) typically maintain rates in the single digits. Here’s a breakdown of average utilization rates by credit score range:

Poor (300–579): ~82.1% or higher

Fair (580–669): ~56.1%

Good (670–739): ~35.2%

Very Good (740–799): ~14.7%

Exceptional (800–850): ~6.5%

While 30% is often cited as a threshold where utilization begins to harm your score more significantly, aiming for 10% or lower can maximize your credit score potential. Interestingly, a 0% utilization rate isn’t ideal, as it suggests you’re not using your credit, which can make it harder for scoring models to evaluate your credit behavior. A rate of 1–10% demonstrates responsible usage without overextending your credit.

How Credit Utilization Impacts Your Credit Score

Credit utilization is a major component of most credit scoring models, accounting for approximately 20–30% of your score. Its influence manifests in several ways:

Overall and Per-Account Utilization: Both your total utilization rate and the highest rate on an individual account can affect your score.

Recent Data Focus: Most scoring models prioritize the latest reported balances and limits, meaning paying down balances can quickly improve your score.

Trending Data in Newer Models: Advanced models like VantageScore 4.0 and FICO 10 T analyze utilization trends over time, rewarding consistent low usage.

The precise impact of utilization depends on your current score, the scoring model, and other factors in your credit report. Generally, lower utilization correlates with higher scores, making it a powerful lever for credit improvement.

Reducing your credit utilization rate involves either decreasing your balances or increasing your available credit. Here are practical strategies to achieve this:

Pay Balances Early: Credit card issuers typically report balances at the end of your statement period. Making payments before this date can lower the reported balance, reducing your utilization rate.

Request Higher Credit Limits: Contact your card issuer to request a credit limit increase, especially if you’ve demonstrated timely payments or increased your income. Be aware that some requests may trigger a hard inquiry, which could temporarily ding your score.

Update Your Income: Inform your card issuer of income increases, as this may prompt them to raise your credit limit automatically.

Consolidate Debt with an Installment Loan: Use a personal or home equity loan to pay off revolving debt, lowering your utilization rate and potentially securing a fixed interest rate.

Open New Credit Lines Cautiously: A new credit card can increase your total available credit, but avoid opening accounts solely for this purpose, as new accounts may lower your score temporarily.

Keep Old Accounts Open: Closing a credit card reduces your available credit, increasing your utilization rate. If the card has no annual fee, consider keeping it open and using it occasionally to keep it active.

Budget for Low Utilization: Estimate your monthly credit card spending, multiply by 10, and aim to have that amount as your total available credit. This keeps your utilization around 10% without needing to time payments.

Issuers typically report balances to credit bureaus at the end of each statement period, coinciding with when your statement is generated. Your payment due date is usually a few weeks later.

Closing a card reduces your total available credit, which can increase your utilization rate. If possible, keep cards open or switch to a no-fee version to preserve your credit limit.

A 30% utilization rate is better than higher rates, but it’s not optimal. Those with top-tier credit scores typically maintain rates below 10%, so aiming lower can further enhance your score.

Most credit scores reflect only your most recent utilization rate, so lowering it can quickly improve your score. However, newer models that track trends may consider past utilization, making consistent low rates beneficial.

You can track your credit utilization by accessing your free Experian credit report, which provides balances and limits for your revolving accounts. Use this data to calculate your overall and per-account utilization rates and monitor changes over time. Experian’s FICO Score monitoring can also alert you to significant shifts in your credit profile, helping you stay on top of your financial health.

By understanding and managing your credit utilization rate, you can take control of a critical aspect of your credit score, paving the way for better financial opportunities.